Thanks!

The new conditions are quite hard

• 50.1% equity

• limited mortgage sum, market price for exceeding amount

max. Moscow 12mil

max. Rural 6mil

• only families

• only new builings/ in construction/ in the planning

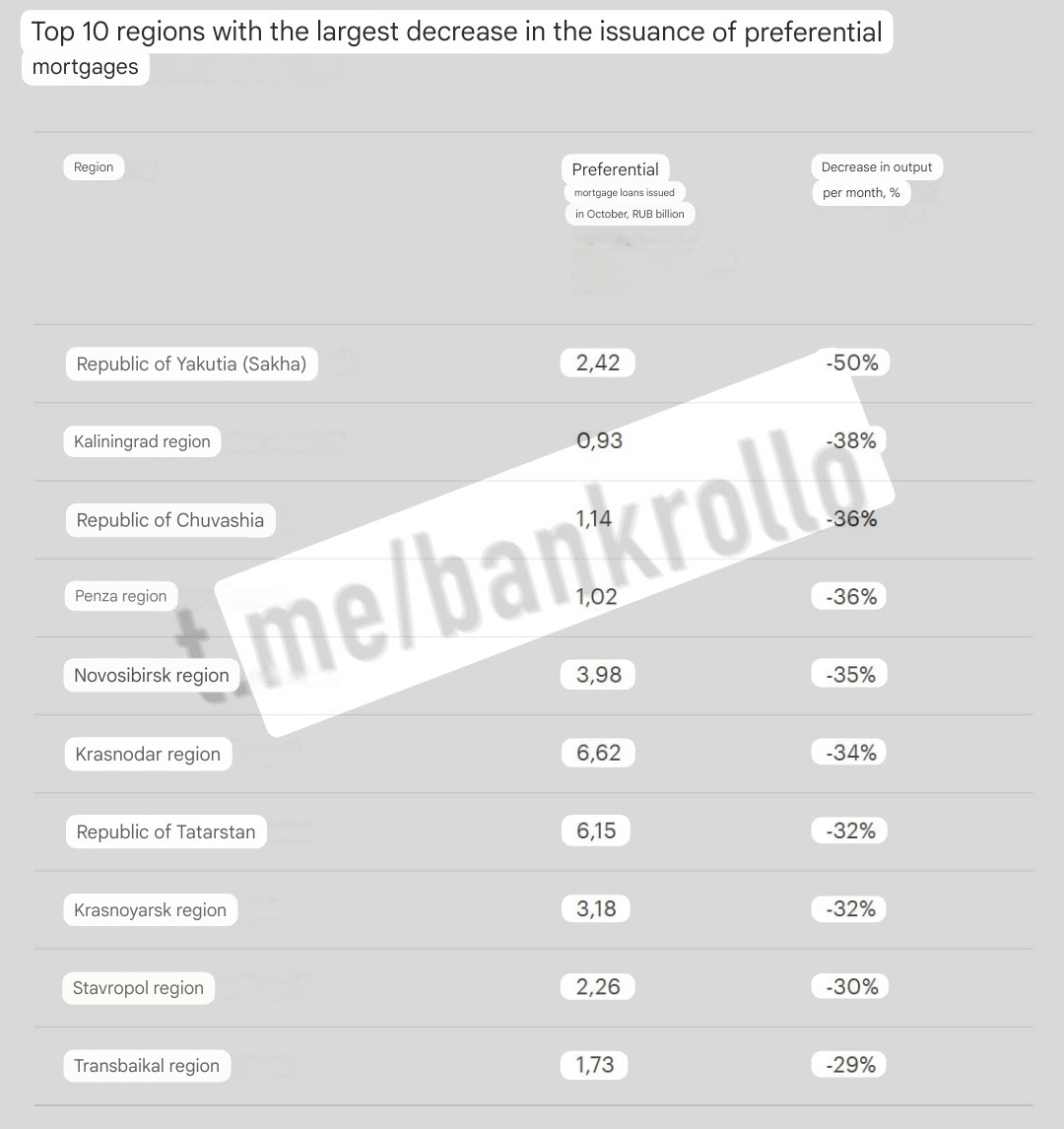

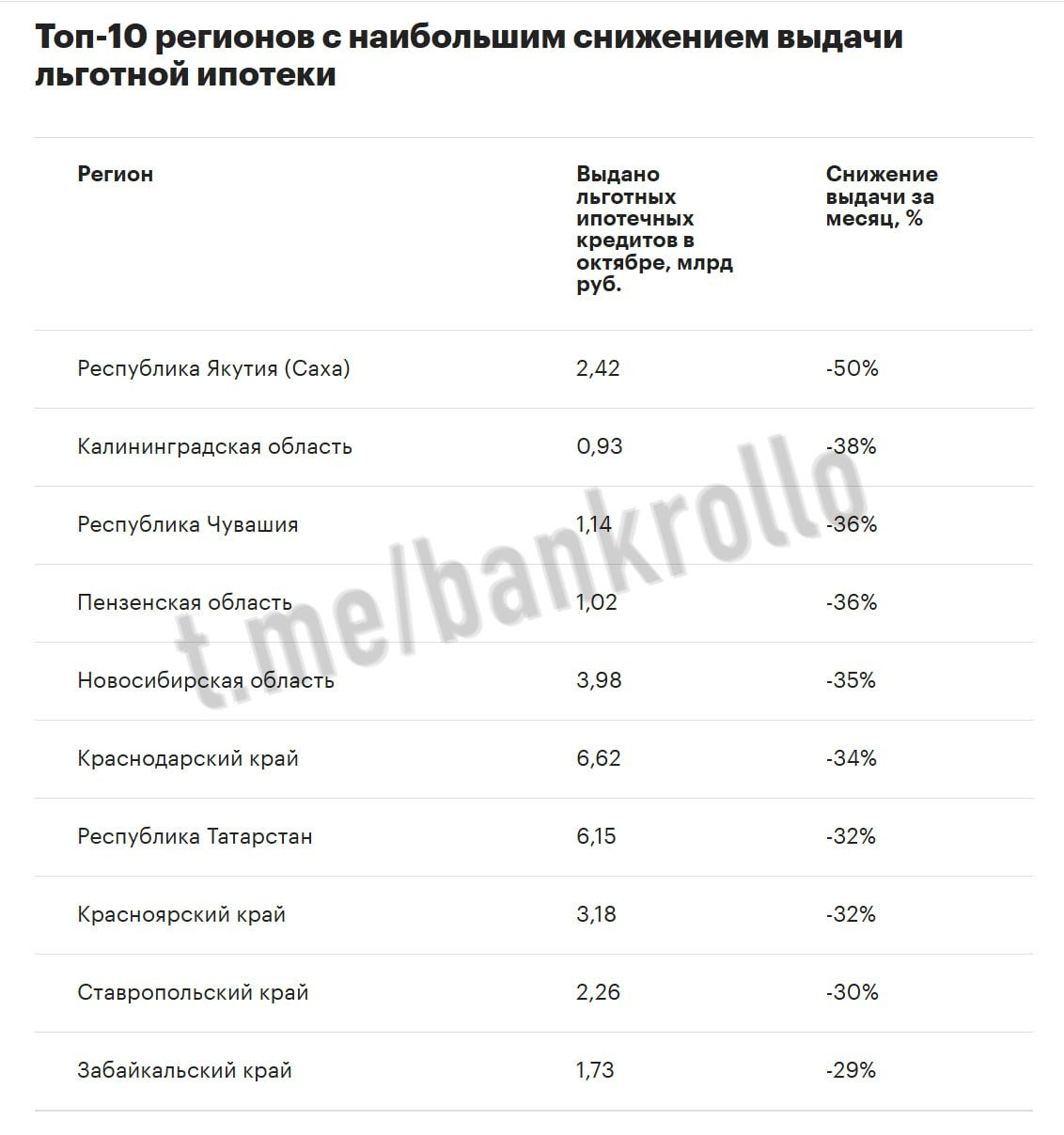

Yes, with this conditions it’s almost impossible. You can see also on the very low volume. Even richer regions like Krasnodar or Tatarstan has overall about $60 Million total mortgages. This why I would take a look on the overall statistics.

When people stop buying homes, they also stop moving. Thats sounds like USSR where you would need a permission to move to another region. I say within 2 years everything is nationalized and within 5 years they are like NorthKorea. Does Putler have an Heir?

If Putin had just put his efforts into improving Russia and improving the lives of the Russians instead of trying to expand his country via war, slaughter, and destruction ...

Are russian mortgages for the length of the amortization — say, 25 years at 8% — or do they have to be renewed, with a new interest rate, after a set number of years?

Because having to renew at 28% could do some damage.

I still have to find out.

Somewhere I saw amortization in RU of 30 years, rather unusual for the West. In CH we have 1st and 2nd mortgage, seen nowhere but in CH.

All that makes quite a difference.

Thx to remind me.

Good question. In Norway mortages are traditionally floating, that is the Norwegian Interbank Offered Rate (NIBOR) + some points. Don't think this is the case in Russia. I don't know what was considered a normal rate a few years back. Guess most households would struggle if rate went 4 -> 28%.

These are "preferred" mortgages, ie subsidized by government, ie relatively affordable. What this chart shows is that the government has run out of money to continue subsidizing such mortgages. Hence the drop.

Good. We could probably stop the war quicker by collapsing the russian economy than we could on the battlefield. Next... go after the shadow oil tanker fleet

The faster the russian economy collapses, the better.

And the USA better not save their asses for a third time; this time they can feel a little pain for a decade or two.

... and if you want to sell your property, you will only find a buyer at a very, very low price. Many who can no longer pay their loan (because of variable interest rates) will lose everything & still be in debt - and the property market will continue to collapse.

Comments

They were frozen at 8% but are not available any more.

https://www.themoscowtimes.com/2024/10/18/russias-real-estate-market-rocked-by-the-end-of-generous-mortgage-subsidies-a86738

https://www.sberbank.com/ru/person/blog/vidi-lgotnoi-ipoteki

The new conditions are quite hard

• 50.1% equity

• limited mortgage sum, market price for exceeding amount

max. Moscow 12mil

max. Rural 6mil

• only families

• only new builings/ in construction/ in the planning

1-Bedroom, 33m2 about 10mil (no family), 30km to Centre M

2-Bedroom, 50m2 abt 13mil, 35km to Centre of Moscow

Quite a challenge.

or peasantry like under tsars

Their elections are a total farce.

28% for mortgages

21% key interest rate, Oct 24

https://tradingeconomics.com/russia/interest-rate

Because having to renew at 28% could do some damage.

Somewhere I saw amortization in RU of 30 years, rather unusual for the West. In CH we have 1st and 2nd mortgage, seen nowhere but in CH.

All that makes quite a difference.

Thx to remind me.

We also have 2nd mortgages, but the rates can be much, much, higher.

Can we speed that up in any way?

And the USA better not save their asses for a third time; this time they can feel a little pain for a decade or two.