How about we remove the term climate change from legislation current and future. Shit! Floriduh Freedumb already did! I know, let's call it building resiliency. I say from what? They say, "You know, we can't say those 2 words".....oh the inhumanity!

Floriduh will stop them. Passing some more free speech prohibitions. Remember what Gov Mo-Ron says: you're as free as I say you are. Floriduh Freedumb!

as if they (or anyone) have the data to accurately predict it. When it comes to data, garbage in/garbage out. What did it come up with for all of the homes in NC that were destroyed this year hundreds of miles from a coastline?

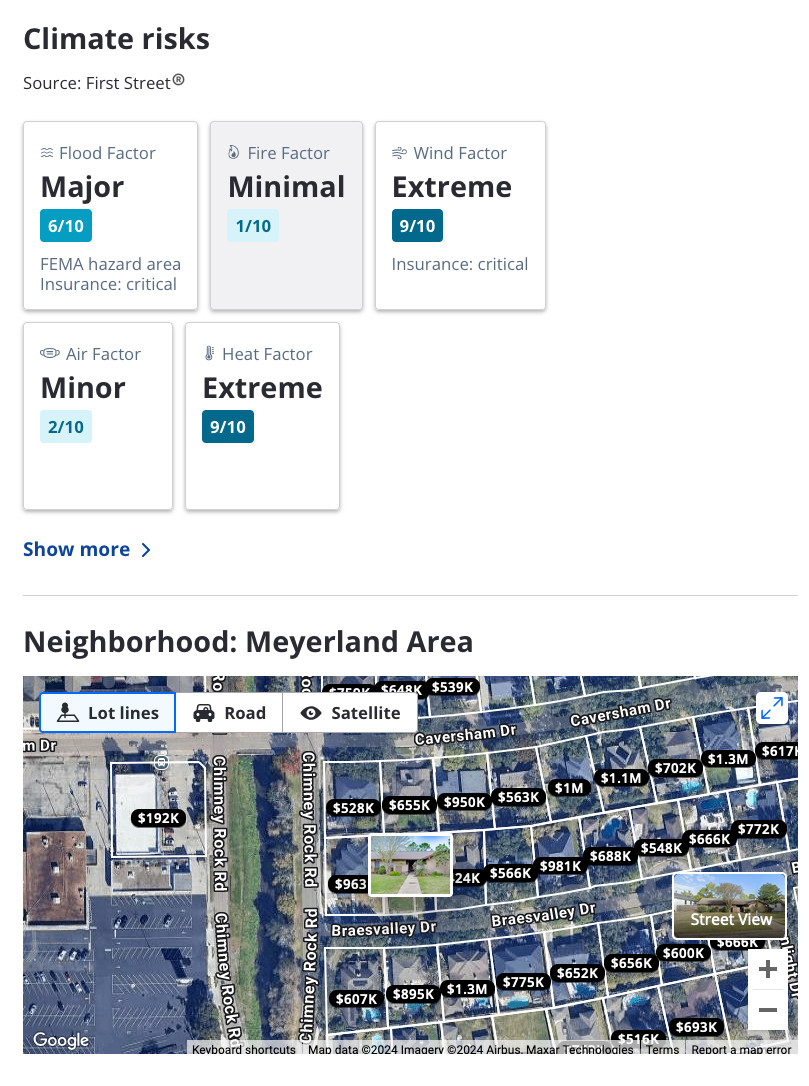

on the other hand, not everything zillow does is helpful. this house (about a block from where I grew up in Meyerland), is extremely likely to flood in the next big event in Houston. the home insurance number is just fantasy. where in the world did they get it? https://www.zillow.com/homedetails/5246-Braesvalley-Dr-Houston-TX-77096/28084196_zpid/

Those climate risks are from First Street; Zillow doesn't have the details on those per house risks and won't. I guess the actual insurance risks will have to be reviewed on a house-by-house basis, sales agent should get estimates. Also, no climate risk in low risk areas (e.g., ZIP 97212).

No doubt the insurance industry, especially re-insurer Munich Re is a factor here.

Jacking up the beach house is only for the uber-wealthy of course. Because no insurance company will cover those anymore, not matter how much jacked up

This is why we sold in the Panhandle and the tf out of FL. Our house was 8 ft above sea level and escaped a flood by an inch, the last hurricane. Nope!

But the whole area will still be flooded and that is a huge problem or am I missing something here? Infrastructure and daily necessities are still at huge risk that will for sure impact the liveability of the place?

Shoutout to Ali Mostafavi at TAMU who's been doing a lot of engineering research on infrastructure vulnerabilities to extreme weather events in Houston and elsewhere.

His work addresses impacts on daily living needs, access by first responders, etc.

Yeah I look at an area for flood risk, not the individual property. Obviously being in a flood risk area is the data buyers should have, then they can assess for themselves or with an expert whether the property is built for resilience and whether the purchase is worth the risk.

certainly the flood risk for a particular property can be different from the flood risk for the neighborhood as a whole. both are useful and I'd be interested in having separate metrics for each.

Yes, this is exactly the problem with "risk communication" based only on maps and public info -- no consideration for the structure itself.

CA's mandatory nat haz disclosures have the same problem, and the seismic "checklist" invented to solve it does not work at all (ahem, realtors).

they don't, for the most part, or are restricted to a rear, ramped garage entrance if there is one. Goodness help the homeowner who becomes a wheelchair user after they've bought the house.

exactly this. even hurricane insurance doesn't cover flood. insurers do not want to cover floods in areas that are even a little susceptible to flooding; it has to be offered (and subsidized) by the government.

I’m glad you’re talking about error analysis. This brings to mind the fiasco a few years back where Zillow relied on predictive modeling to purchase real estate, ended up making some bad bets, and had to lay off a bunch of folks. Not the best track record.

Zillo obtains flood risk from First Street Foundation, which uses probabilistic modeling rather than deterministic physical modeling. First Street's NATIONAL model is very rough. It considers ground elevation (not finished floor), distance to open water, and similar geographic info.

Since their site first opened up to the public ~4 years (?) ago, First Street’s model has (correctly) ratcheted up the ember storm risk throughout my town. At first, my house’s wildfire risk was “3”; now, it’s “7.” Should homebuyers assume that F.S.’s models will continue to tweak risk estimates? 🔥

It suggests there is actual consumer demand for this information (how valuable this rating will be is certainly an open question) - could be there is more of an awareness shift at the individual than polling would have us believe?

I would expect insurers, and especially re-insurance they are doing their own risk analysis have their own models - though maybe they like this as a way to send price signals to the market for justifying policy cost variance?

On the buyer side, I also suspect the insurance issues in places like Florida and California due to flood/hurricanes/fires have risen awareness to the point that it is has become commonly requested data.

People really need to think of the three little pigs when buying property. Lots can be changed about a building, but the local environment is not feasible subject to your desires.

When my wife found the house she wanted, I went to Google Earth to look at the lay of the land to see whether it's in a flood risk zone. I looked at the elevation--near the top of a low hill, and considered its distance from creeks and streams. It's also away from urban-wildland interfaces.

Yeah we had been living in an older part of Sacramento where all the apartment buildings are historically built up 2 feet above ground level for a very good reason. Made me nervous every time a big atmospheric river came through. Decided I wasn't going to repeat that anxiety for the permanent abode.

Royal Lepage in Canada has had climate risk data for quite some time and I was very impressed when they added it. That’s only a specific realty company though, not the national database

This was very important when we were last looking at houses. Flood risk is very variable in our surrounding area (lots of hills and creeks). Checking local news coverage also helped give us an idea of what infrastructure issues were likely in the event of flooding.

But it's worth noting that house pricing doesn't seem to be impacted, at least in our area. (There are some houses with high flooding risk I'd've otherwise been interested in, and they got snapped up at the area's general market rate.)

Redfin was doing it for quite a few years---using the same source, https://firststreet.org/ First Street does good climate analysis and prediction for all who... want and can afford it (public policy shops, shipping companies, investors, institutional finance, you name it)

first street does not rate my house properly. I am on a hill and border a creek at the bottom of that hill, which does flood out my neighbor on the other side. yet we are ranked the same.

its not. it doesn't see elevation. it assumes, for my house, that I am at the same elevation as the guy on the other side of the creek and doesn't see that I am on a hill

We've bought 2 houses in the past decade. In both cases we looked at weather, sea level, flood plains, forest fires, etc, etc. It's a massive investment and shouldn't be assumed that insurance will cover if you buy somewhere stupid.

Oh, hey, Andy. Shouldn’t have been surprised to find you on this thread.

Clicked because of seeing Meyerland. Think about this often in Chicago. We’re in a good space by happenstance for flooding, at the top of the rise from Lake Michigan which, in turn, unlikely to rise much.

hi Hal. Sadly, no one will escape climate change. But some people will be better off than others. I always thought that the Great Lakes region would be among the best places to be.

It definitely feels that way between wildfires and hurricanes, but, yeah, we’ll get hit too. When I hear neighbors crow how awesome it is they don’t really have to shovel snow anymore, I just have to roll my eyes.

Redfin does this, too. One of the fascinating things about looking for a house in the West is the "air factor" because most of that is the annual smoke blanket.

GOP govt sets a policy to not include climate crisis in fed planning policies, staff tries to use other vocab. Doge would close down NOAA? Climate crisis outpacing science projections. Quite a % of homeowners free of mortgage are dropping insurance? Caution: rosemary plants ignite very volatilely.

They should. Existing flood hazard should be disclosed for all properties. Repeat flood damage should be required disclosure for all properties. Fluvial hazard zone should be mapped for all properties.

Who does not want the hazards known? People making money off building in hazard areas.

You can’t see your house but look in your neighborhood for a house on sale then go to the map. You can zoom out around to your house and see the data that way

Folks in FL are discovering that already. Insurance companies are very reluctant to take on homeowners there now, thanks to both the hurricane/flooding danger and the way the state government is sweeping it all under the rug.

Yes and what makes it a challenge is that even if people make the connection between insurability and climate will they start to vote for climate? Even if we started to make bold moves to address climate change these weather disruptions are going to continue to get worse for some time. /1

They need to be worried about insuring their homes but they also need to worry about even just the viability of their homes & the livability of the planet for their children & grandchildren. Can people make decisions today where the full impact of those decisions will not be felt until years later?

https://Realtor.com does a similar thing. Used it to evaluate our flood risk for our new home and it looked pretty reasonable given I know the area well.

Due to my experience of false online info (provided by FirstStreetFoundation last year), I will NOT look to them for facts. I could not get Redfin or Realtor .com to correct their websites on flood risk from FirstStreet. Realtors utilize 3rd party natural hazard disclosure reports in CA for facts.

We've been house shopping. For the first time with our home moves I've been consulting our insurance broker for quotes on prospective homes. We ruled one out as a result, premium was substantial and they mentioned red flags. All climate related with some insurers refusing coverage.

100% agree. I would never buy a house without getting an insurance quote. Of course, that’s no guarantee that rates won’t go up and become unaffordable later …

Best advice taught by an owner/broker of waterfront properties was always provide a 100 year flood plain history.

Don’t have the name of an international insurance group out of Switzerland area that forecasts global warming trends, but it’s taken into account for underwriting rates.

This is great news! By allowing some to ignore the climate and climate change when building and buying housing has caused all of us to pay higher insurance premiums.

Wow. Have seen other RE sites which show flood /noise risk , but Zillow isn’t downplaying a major why. Good for them, altho too many will still naysay it

Finally, a step in the right direction! Zillow adding climate risk is HUGE—this is about time. If we want to make smart investments and protect future generations, we need to face the truth. It’s called being responsible, something this country has lacked for too long!

Interesting! Picture Miami flood risk. I live in the Netherlands but our Zillow, Funda does not add these climate info (yet). @nu.nl @volkskrant.nl Interesting?

Very smart. Those of us who have functioning brain cells and believe in climate change already pay attention to climate factors/risks when investing in a property. Perhaps this will help deniers better understand what they may be getting themselves into before Floriduh sinks into the ocean.

Brisbane City Council mapped the entire city after the '74 floods and provided an economical search service on flood possibilities and mitigation to would be buyers.

This service was quickly challenged by commercial interests, and very good information was locked away and 'lost'.

realtor and redfin do it, too! it’s unavailable on some properties, and idk if it’s missing data or if you can opt out ot what. they’re all sourced from first street, i think, so that’s probably why it’s just based on the maps and not the current state of the property.

Now I'd like for them to put the EUI, energy use intensity on the homes they're trying to help sell too.

Utilities are the second largest cost of owning a building. I think that potential buyers should know how much more one will cost to keep warm & cool over their other options.

redfin was doing it first--zillow started this several months ago, i LOVE it and it has removed a lot of houses from my saved list due to flooding issues.

The detailed subscription report divulged that the area is flood prone, but the house itself is only at .2% risk of water getting in the first floor within the next 30 years.

I went to a reinsurance conference last year and heard basically the same thing: in years when we don’t have a big hurricane, the biggest impacts are from severe convective storms (due to wind, hail, rain).

Kind of interesting, but seems wildly inaccurate. I compared the heat rating - they said Midland Tex was at a lower heat climate risk than Northern Virginia.

Also said the high temp days would be the same in Midland as No Va when a quick look says they are currently at 2-3X the number already. kind of whack execution, but a good thought and hopefully it gets better over time.

Interesting…

I’ve had a theory for a long time that insurance companies will be the first big institutions to believe in climate change enough to take action. Of course, the actions they are taking are cancelling insurance or making it unaffordable in certain areas. Nothing that actually helps.

This data set is confusing me. In air quality, our area is projected to see a 9% increase over 30 years. That's a major risk. While our heat risk goes up by 171% and that's a moderate risk?

Also, urban areas are seen as immune to wild fire?

I applaud adding the data. I question the data.

Realtor dot com has an environmental risks section under any property you look at on it. I told my fiancée I won’t even consider a house unless the flood risk is minimal.

this is a problem for me. my house is on a hill. at the BOTTOM of the hill is a small creek that occasionally overflows with heavy rains, flooding the other side which is a flat plain, and he requires flood insurance. but 1st Street assumes it is all flat and that I have the same risk. NOT.

Yes, It is a big deal, and it can also be really misleading. A lot of climate risk models are based on low resolution and out of data public data sources. This can lead to a lot of problems, for instance...

Climate regulations in many place now require climate risk disclosures. There are plenty of mid sized companies without much experience with compliance protocols. Combine this with a marketplace full of products with black-box algorithms and data, unverified quality, and prices all over the map.

It will not be long until enterprising people tasked with doing climate risk disclosures realize that they can just find the risk score of homes on Zillow near their company locations, and publish them. They will end up in quarterly reports and be used to identify some risk for valuing the companies

In some cases, they may end up dangerously wrong. I'm aware of a situation where a global company was told by one of the biggest climate risk vendors that a specific factory had 0% risk of 100 year flood just weeks after suffering a 100 year flood.

This can happen for a lot of reasons. For instance, most systems look at risk averages in geographic grids, similar to google maps. Everything in an area, say 50km², gets the same score for each specific risk, like fire, flood, etc. based on averaging the data. (generalizing here a bit of course)

Buildings on the shore of a river 250ft below the average elevation of the rest of that region get the same flood score. Oops! things now appear to have a lot less risk than they actually do. At a high level, this system is probably performing ok. But if your job is to understand your actual risk,

Comments

(lived here my whole life)

And, a lot of the houses on the market further north (in our price range) seem to have no defensible space anywhere around and are built to burn.

Alt: own a few goats. 😁

Coastal houses burn fast since they're packed tight. One goes up they all go.

Also the Maui fires.

I supposed I can burn fossil fuels to my heart's content now!

Problem solved.

it could easily cost the owner of a home with high climate risk tens of thousands of dollars.

https://www.zillow.com/homedetails/5246-Braesvalley-Dr-Houston-TX-77096/28084196_zpid/

https://www.nytimes.com/2024/12/27/realestate/home-lifts-flooding-climate-change.html?unlocked_article_code=1.lE4.ymy_.otjcCv7jTKXd&smid=url-share

Jacking up the beach house is only for the uber-wealthy of course. Because no insurance company will cover those anymore, not matter how much jacked up

yeah, gotta give credit where it's due, and it should be reflected in the value.

have you seen any analogues for fire risk?

His work addresses impacts on daily living needs, access by first responders, etc.

https://engineering.tamu.edu/civil/profiles/mostafavi-ali.html

A lot of heavy water coming through is gonna push those over, and might cause a lot more force against whatever supports are underneath

CA's mandatory nat haz disclosures have the same problem, and the seismic "checklist" invented to solve it does not work at all (ahem, realtors).

I remember one house did it after a flood in the 90s and was the only one for years. Not anymore.

https://www.fema.gov/flood-insurance

Terrible that has to be mentioned on every house(however ive experienced floods since I lived in my house just stopped after Summer in 2018.)

Clicked because of seeing Meyerland. Think about this often in Chicago. We’re in a good space by happenstance for flooding, at the top of the rise from Lake Michigan which, in turn, unlikely to rise much.

I'll never buy a house (lol) but how is this not THE FIRST question people ask??? You are taking out 3/4 of a million dollars in 30-year debt!

the tree in my living room last month begs differ

Who does not want the hazards known? People making money off building in hazard areas.

I’m less worried about my home flooding than my surrounding area, but still

Would be major mal practice for them to NOT do this

Don’t have the name of an international insurance group out of Switzerland area that forecasts global warming trends, but it’s taken into account for underwriting rates.

If Zillow's info doesn't match FEMA's or NFIP's info, they will be sued.

https://eos.org/opinions/do-you-know-your-homes-flood-risk

This service was quickly challenged by commercial interests, and very good information was locked away and 'lost'.

Utilities are the second largest cost of owning a building. I think that potential buyers should know how much more one will cost to keep warm & cool over their other options.

btw they link to this site:

https://firststreet.org/

We almost passed up a place we really loved because the flood risk on Redfin said « major »

We got the house.

I’ve had a theory for a long time that insurance companies will be the first big institutions to believe in climate change enough to take action. Of course, the actions they are taking are cancelling insurance or making it unaffordable in certain areas. Nothing that actually helps.

Also, urban areas are seen as immune to wild fire?

I applaud adding the data. I question the data.